Companies acquiring rights to extract natural resources like oil, minerals, and timber need to estimate the total available resources. Thus, authorities allow these companies to charge a tax-deductible expense for extracting these resources (depletion charge). For loan amortization, the borrower will multiply the depreciation vs amortization loan amount by the interest rate.

- Demand goes through the roof, the machine is put to the test, and it produces a whopping 15,000 mugs.

- Business startup costs and organizational costs are a special kind of business asset that must be amortized over 15 years.

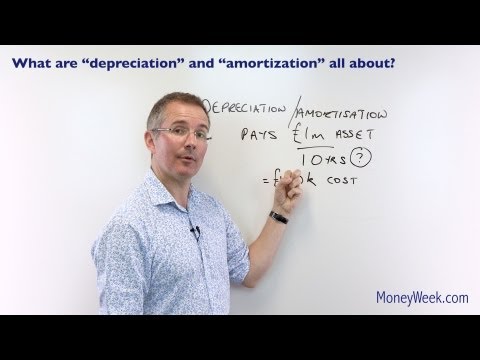

- The key difference between depreciation and amortization is the type of asset that’s being expensed.

- This method uses a fraction to calculate the asset’s rate of depreciation for each year.

Types of Assets

- The main differences are in the types of assets they account for, as depreciation covers physical assets while amortization covers non-physical assets.

- Both depreciation and amortization have a direct impact on the balance sheet.

- For intangible assets, the estimated economic value is based on factors such as the asset’s remaining legal life, market demand, and other factors.

- Each year, depending on the use and economy, an accountant will need to evaluate the price difference of each asset and add it to the balance sheet.

The straight-line method is one of the simplest and most commonly used approaches for software depreciation, involving evenly spreading the cost of the software over its useful life. If you plan to buy new equipment, vehicles, or software, discuss the best way to handle the deductions with your tax advisor or accountant. This means the company will record a depreciation expense of $5,000 annually for five years, reflecting the van’s diminishing value over time.

Accelerated Amortization

- As mentioned above, a business can amortize the full cost of an intangible asset at the same rate each year throughout the asset’s useful life.

- The concept is used, among other things, to reduce the taxes a company pays.

- The strategic use of these accounting concepts could ease current tax obligations and improve cash flows, making them particularly advantageous for clients.

- This means a portion of the asset’s cost can be deducted each year from the business’s taxable income, lowering the tax bill.

- On the other hand, amortization expense reduces the carrying value of intangible assets with an identifiable life, such as intellectual property (IP), copyright, and customer lists.

Proprietary processes are amortized over their useful life, which is typically years. Amortization is used to spread out the cost of an intangible asset over time, while depreciation is used to spread out the cost of a Bookkeeping for Startups tangible asset over time. Let’s say you purchase a license for $10,000 and the license will expire in 10 years. Since the license is an intangible asset, it would have no salvage value, so the full cost would be amortized over that 10-year period.

What is the Journal Entry to Record Amortization of an Intangible Asset?

Governed by accounting standards such as GAAP or IFRS, specifying how intangible assets should be amortized. Depreciation and amortization are fundamental concepts in accounting and finance, essential for accurate financial reporting, tax planning, and business strategy. Understanding the differences and similarities between these processes enables businesses to make informed decisions, optimize their financial performance, and comply with regulatory requirements. This total reflects how the company allocates the cost of both tangible and intangible assets over their respective useful lives.

Amortization applies to intangible assets, while depreciation applies to tangible assets. In contrast to tangible assets that physically wear out, intangible assets lose value either because of the expiration of legal rights or by becoming technologically or commercially https://www.bookstime.com/ obsolete. Amortization expense is an important factor in financial reporting because it accurately represents the decreasing value of intangible assets over a period of time. This gives an insight into the actual financial performance of a company regarding the expenses incurred in maintaining and using intangible assets. The most significant difference between the two is the type of assets the method is applied to. Depreciation is an accounting method used for fixed assets, while amortization is used for intangible assets.